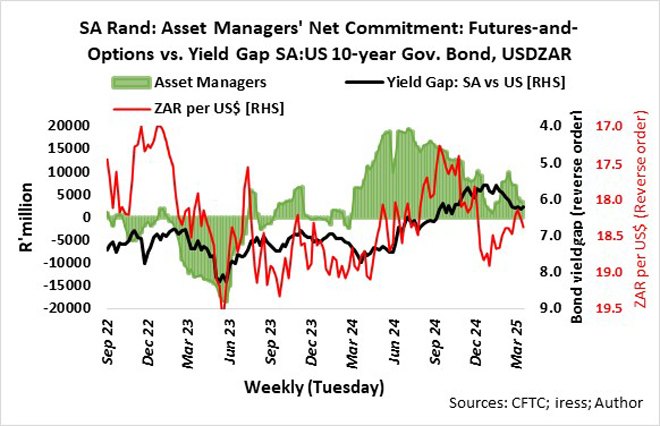

A year ago, one month before South Africa’s general election, foreign asset managers turned bullish on the country after the yield gap between South Africa’s implied 10-year government bond and that of the United States reached 8%.

Statistics published by Commodity Futures Trading Commission indicate that the net combined commitment of asset managers via futures and options to the rand increased by more than R10 billion by the end of September from R6bn at the end of April. Over the same period, the 10-year bond yield gap narrowed to about 6%, while the rand gained 9% against the US dollar. Bond Exchange of South Africa statistics indicate that from the week after the election at the end of May last year until the end of September, net foreign transactions in South African bonds registered net sales of a meagre R39 million.

Foreigners saw the strong rand and narrowing bond yield gap as an opportunity. From the end of September last year until mid-January this year, asset managers gradually reduced their exposure to the rand via futures and options by about R15bn and sold bonds worth about R17bn. This caused the rand to drop by 6% to 18.92 to the US dollar.

Asset managers briefly upped their exposure in February as they took advantage of the major sell-off of the rand but subsequently continued to cut their exposure to the rand, while foreigners were net sellers of SA bonds valued at R61bn since mid-January as the rand rebounded against the greenback.

The selling of SA bonds by foreigners caused the SA-US bond yield gap to increase to 6.2% from 5.6% at the end of January this year, and it is threatening to test previous support at about 7%. As things stand, it is difficult to become or remain bullish on the rand unless something drastic happens, such as the X-factor (no pun intended, Elon Musk).

The X-factor

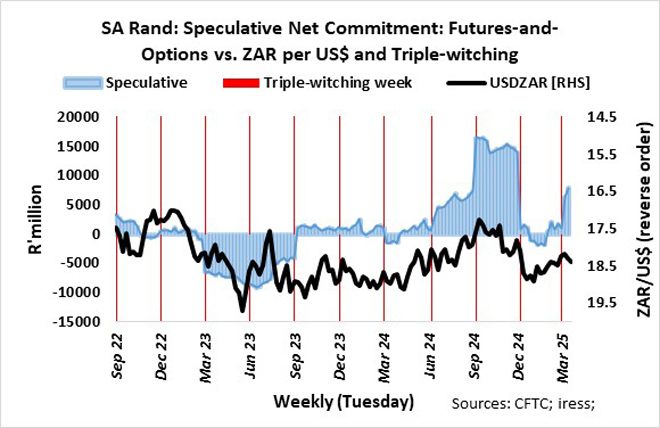

My analysis of speculative positions on the rand was a revelation and perhaps startling. My data analysis of speculative positions on the rand is based on the net commitment of non-commercial traders’ futures and options on the rand published by CME. According to Investopedia, non-commercial traders “are taking positions in the market purely to seek a profit from market moves as a speculator”.

The accompanying graph depicts the net commitment to futures and options of non-commercial traders in regard to the rand against the rand exchange rate to the US dollar as well as triple-witching weeks. “Triple witching refers to the near-simultaneous expiration, on the third Friday of every third month (March, June, September, and December), of three different types of derivatives” (Britannica Money) – namely, stock options, stock index futures, and stock index options.

Three distinct periods can be observed.

On 14 March 2023, a speculative net short position (negative net commitment) of R6.5bn was recorded. The initial rand weakness was sparked by asset managers going heavily short on the rand.

On 12 September 2023, a speculative net short position of R4bn was recorded. The position was closed after the reporting date. There was no apparent effect on the rand’s exchange rate to the US dollar.

Speculative net long positions increased steadily to R7.4bn on 10 September 2024 from R672m on 18 June 2024. On 17 September 2024, speculative net long positions surged to R16.5bn. The rand strengthened to 17.26 against the US dollar a week after the recording date from 17.94 a week before the recording date.

On 17 December 2024, speculative net long positions fell by R13bn to R700m from a week prior. The rand weakened to 18.64 against the US dollar a week after the recording date from 17.82 a week before the recording date.

On 18 March 2025, a speculative net long position (positive net commitment) of R6.4bn was recorded, up from R1.1bn a week earlier. The rand was relatively unchanged against the US dollar before or after the recording date.

From the above, it is evident that the rand’s exchange rate against the US dollar can sometimes be heavily influenced by interested parties, whoever they may be and for whatever reason, specifically around triple witching. The impact can be wide-ranging – from the pricing of securities (stocks and bonds), the external value of the rand versus currencies excluding the US dollar, the monetary translation of assets, and South Africa’s monetary and even fiscal policies.

Furthermore, the influence can make a mockery of commentaries and forecasts, whether they are political or economic.

So, while I find it difficult to get very bullish on the rand, I cannot ignore the bullishness of speculators as reflected in their current net long position in futures and options on the rand.

Yes, the rand is more than meets the eye.

Ryk de Klerk is an independent investment analyst.

Disclaimer: The views expressed in this article are those of the writer and are not necessarily shared by Moonstone Information Refinery or its sister companies. The information in this article does not constitute investment or financial planning advice that is appropriate for every individual’s needs and circumstances.

Thanks for sharing Ryk. Should be of much value for commercial investors.

Very informative for a pensioner who needs to buy dollars for the next overseas visit or cruise.