The latest Sanlam Benchmark Survey highlights a significant increase in respondents planning to withdraw some of their retirement savings under the new two-pot retirement system, rising from 31% in 2022 to 59% in 2024.

The two-pot system, effective from 1 September, will allow retirement fund members to make partial withdrawals from their funds before retirement, while preserving a portion that can be accessed only at retirement.

Koketso Mahlalela, the head of Member-led Outcomes at Sanlam Corporate, expressed concern over this statistic in the Sanlam Benchmark 2024 Insights Report. She emphasised that early withdrawals could jeopardise retirement savings and leave individuals financially vulnerable.

The latest Benchmark Survey included 1 317 consumers, 10 professional interviews, four focus groups, and insights from 16 employee benefits consultants, alongside data from 100 standalone and union funds, and 100 employers in umbrella funds.

Mahlalela cautioned that although the savings component can be accessed in emergencies, it should be used sparingly to preserve retirement provisions.

She noted that for many South Africans, retirement funds are their sole savings, especially amid financial the strain exacerbated by the Covid-19 lockdown.

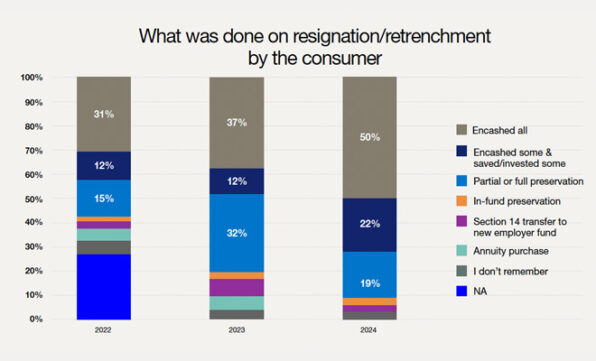

Benchmark Survey data from the past three years examined how consumers spent cashed-out funds upon resignation or retrenchment. While the findings underscore the importance of the two-pot system, they also suggest that if past trends continue, fund members may not access their savings pot as prudently as recommended.

The table shows that in 2024 only 19% of those who were able to access some of their funds on resignation or retrenchment preserved their funds when changing jobs.

“This is alarming, given that in 2023, 32% of members would have preserved some or all of their funds on withdrawal from their fund. The fact that in 2024, 50% of individuals opted to cash in all their retirement funds – a step backwards from the 37% of consumers that cashed in their funds in 2023 – emphasises the increasing financial pressures consumers are facing.”

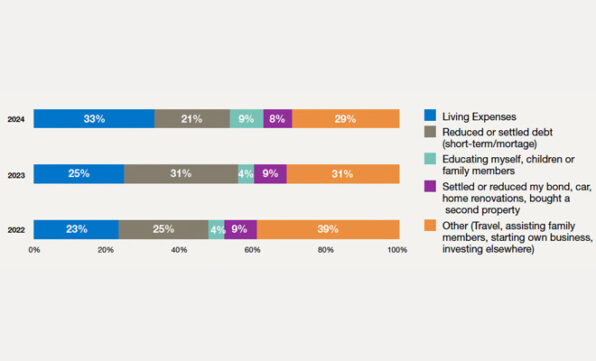

Mahlalela says it is also important to understand how these encashed funds were spent.

In 2022 and 2023, most respondents opted to use the encashed funds to service, reduce, or settle their debt. A second trend was to use the encashed benefits to manage their living expenses. In 2024, the spend on living expenses shot up to 33% of survey respondents.

“Some of the funds were also used for educational purposes or for asset maintenance. Twenty-nine percent of respondents used the encashed benefits for other diverse purposes. The main need for additional funding appears to be to manage debt and more recently to meet day-to-day living expenses,” she says

To help employees balance building robust retirement savings with managing financial distress, Mahlalela suggests employers should offer alternatives to accessing their two-pot savings. These could include rewards and loyalty programmes, money management tools, debt management assistance, and access to financial advice.

Financial education and advice

Mahlalela underscores the critical need for financial education on the two-pot system and its implications to ensure members make informed decisions.

She says it is vital to note that fund rules still govern the vested pot.

“This means the risk remains that an individual could decide to withdraw all his or her funds on resignation or retrenchment, ultimately depleting a significant portion of his or her retirement savings.”

Mahlalela emphasises the role of financial advice in this context.

“A financial adviser will be able to map out members’ specific financial needs, identify gaps, and come up with a financial plan that is best suited to their circumstances, risk, savings, health and other protection needs.”

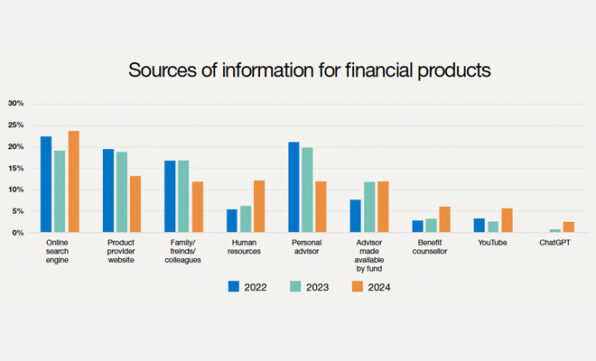

Despite the critical role financial advisers play, the Benchmark Survey shows that when it comes to sources of information for financial products, “personal adviser” has dropped from about 21% in 2022 to about 12% in 2024. More consumers are opting to make use of online search engines (about 24% in 2024) and product provider websites (about 14% in 2024).

“This, however, misses the personal overview of understanding one’s current financial profile or standing, which would have been provided by a financial adviser,” says Mahlalale.

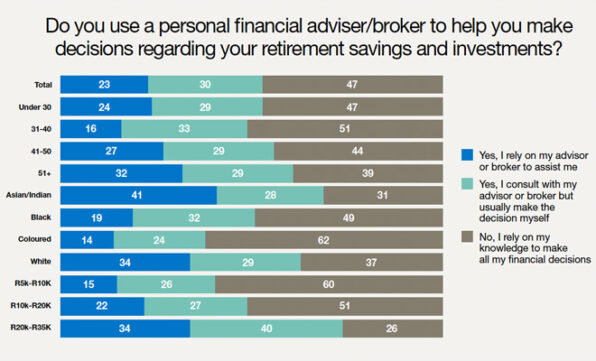

When looking at whether respondents use a personal financial adviser/broker to help them make decisions regarding their retirement savings, 47% of individuals said they relied on their own knowledge to make all their financial decisions.

The tendency not to rely on an adviser or broker for financial decisions is notably high among individuals aged under 30 (47%) and those aged 31 to 40 (51%), as well as in lower-income brackets – 60% in the R5 000 to R10 000 bracket and 51% in the R10 000 to R20 000 bracket.

Mahlalela expresses concern over the 47% of individuals managing financial decisions independently, given the complexity of financial products. She suggests that engaging a contracted or personal financial adviser could help simplify these complexities. Such advisers can also provide guidance on alternatives to withdrawing from the savings pot.

“If individuals understand their financial situation, it will assist the financial adviser to utilise the best alternatives for them based on the financial products available to suit their needs.

“Employers on the fund have contracted financial advisers, making access to financial advice accessible and affordable to members,” she says.