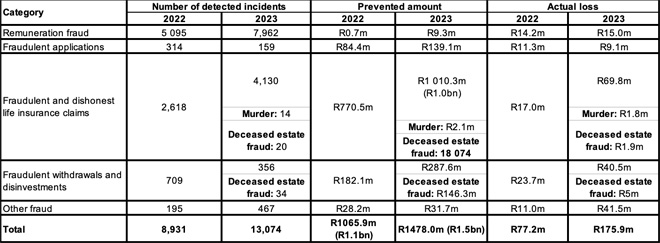

South African life insurers and investment companies detected 13 074 cases of fraud and dishonesty in 2023, a 46% increase from the previous year when 8 931 cases were detected, according to statistics from the Association for Savings and Investment South Africa (ASISA).

The industry lost at least R175.9 million to fraud and dishonesty in 2023, a 128% increase from the R77.2m lost in 2022. The early detection of fraud and dishonesty prevented losses worth R1.5 billion in 2023 compared to R1.1bn in 2022.

ASISA’s Forensic Standing Committee yesterday released its second set of comprehensive fraud statistics for the industry. Following a complete overhaul last year, the statistics cover fraud reported by investment companies in addition to the fraudulent and dishonest claims statistics reported by life insurers.

Jean van Niekerk, the convenor of the Forensic Standing Committee, attributed the steep increase in fraud detected in 2023 to a combination of the following:

- ongoing innovation of detection methods by forensic departments;

- increasingly desperate consumers willing to commit a crime for extra money; and

- criminal syndicates who see life insurers and investment companies as lucrative soft targets.

Fraud and dishonesty by category

The ASISA fraud statistics are divided into five categories:

- Remuneration fraud: Fraudulent attempts by call centre agents, tied agents, or independent financial advisers to benefit from commission and/or fees.

- Fraudulent applications: Fraud and dishonesty committed at the application stage through misrepresentation, non-disclosure, impersonation, or identity theft.

- Fraudulent and dishonest life insurance claims: Fraudulent or dishonest attempts to claim benefits from risk policies such as life and disability cover.

- Fraudulent withdrawals and disinvestments: Accessing investments by fraudulent means from linked investment service providers, collective investment schemes, and retirement funds.

- Other fraud: Examples are fraudulent attempts to obtain investment policy benefits and bribery and corruption.

Van Niekerk said more than half of all fraud cases recorded by ASISA members in 2023 were classified as remuneration fraud, showing a steep upward trend from 2022.

“A positive development is the small increase in actual losses, combined with a significant increase in prevented losses. This indicates that our industry’s prevention methods are delivering results,” he said.

Fraudulent and dishonest life insurance claims were the second-highest contributors to fraud cases in 2023. Losses jumped from R17m in 2022 to R69.8m in 2023, driven largely by fraudulent death claims, Van Niekerk said.

According to Van Niekerk, there was also some good news in the 2023 statistics.

“The numbers show a welcome decline in fraudulent applications and actual losses. At the same time, the value of prevented losses was high, which means there was a real impact in preventing application fraud. This also indicates the persistent threat of fraud that the industry faces.”

There was a decrease in fraudulent withdrawals and investments, but a concerning increase in actual losses recorded, which jumped from R23.7m in 2022 to R40.5m in 2023.

“While the attack rate was lower, the value of prevented and actual fraud increased substantially in 2023,” Van Niekerk said.

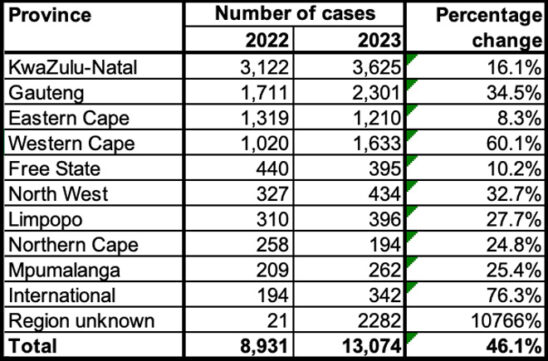

Most fraudulent and dishonest claims in 2023 were uncovered in KwaZulu-Natal, followed by Gauteng, the Western Cape, and the Eastern Cape. The biggest increase in cases by province was recorded in the Western Cape.

Concerning trends

Van Niekerk said two concerning trends that have emerged in recent years are murder for insurance payouts and deceased estate fraud.

“We have requested ASISA members to report on these cases separately, starting with the 2023 statistics, to help our industry find ways to clamp down on these cases with urgency.”

Murder for insurance payouts

Van Niekerk said although criminals often see insurance as a highly lucrative target, cases involving premeditated murder to benefit from an insurance payout are not that common. Of the 4 130 insurance fraud cases reported for 2023, 14 cases related to the involvement of a beneficiary in the insured’s death.

He said the recent case involving a police officer in Limpopo and others such as the Rosemary Ndlovu case have shown that criminals are highly unlikely to get away with this type of crime.

“While life companies pick up on this type of crime very quickly through their data-sharing initiatives, the process of gathering evidence and building a case that will stand up in court is often a slow process. While the Limpopo arrest has occurred recently, the investigation was prompted by an alert from life companies many months ago.”

Deceased estate fraud

Life insurers and investment companies noticed a new trend whereby criminals target deceased estate benefits and investment accounts, Van Niekerk said. In 2023, life insurers reported 20 cases and investment companies 34 cases.

He says deceased estate fraud is committed by impersonating legitimate parties and fabricating letters of executorship and other documents, as well as opening fraudulent bank accounts in the names of beneficiaries by impersonators and false executors.

Most policyholders and beneficiaries are honest

It is vital for the savings and investment industry to ensure that fraud remains in check to prevent fraud-related losses from spiralling out of control and higher claims rates from driving up premiums for honest policyholders, Van Niekerk said.

“Seen in isolation, the fraud statistics paint a bleak picture. However, they should be considered as part of the bigger industry picture, which shows that the majority of policyholders and beneficiaries are honest. This is evidenced by the 95.9% payout rate in 2023 to the beneficiaries of 892 817 life and funeral cover policies to a value of R39.9bn.”

At the end of December 2023, ASISA members managed 43.8 million risk and savings policies and collective investment schemes assets worth R3.5 trillion.

Industry measures to combat financial crime

Many life insurers and investment companies have dedicated forensic departments focused on clamping down on fraud and dishonesty by identifying criminal trends as they emerge, Van Niekerk said.

“A loss of R175.9m to fraud and dishonesty is significant, and our industry is focused on clamping down on criminal activity through continuous evolution and adaptation.”

According to Van Niekerk, preventative measures deployed by life insurers and investment companies include using digital technology such as artificial intelligence, improved industry collaboration, and enhanced authentication mechanisms, such as biometric customer identification.

In addition, forensic departments share data on criminal activity via industry bodies geared to facilitate data sharing to combat fraud and financial crime, including ASISA’s Forensic Standing Committee.

The committee exists to curb fraud by analysing statistics to understand trends, hotspots, and emerging risks at an industry level. The committee also facilitates the industry’s drive to partner with law enforcement agencies and regulators to ensure criminals are brought to book.