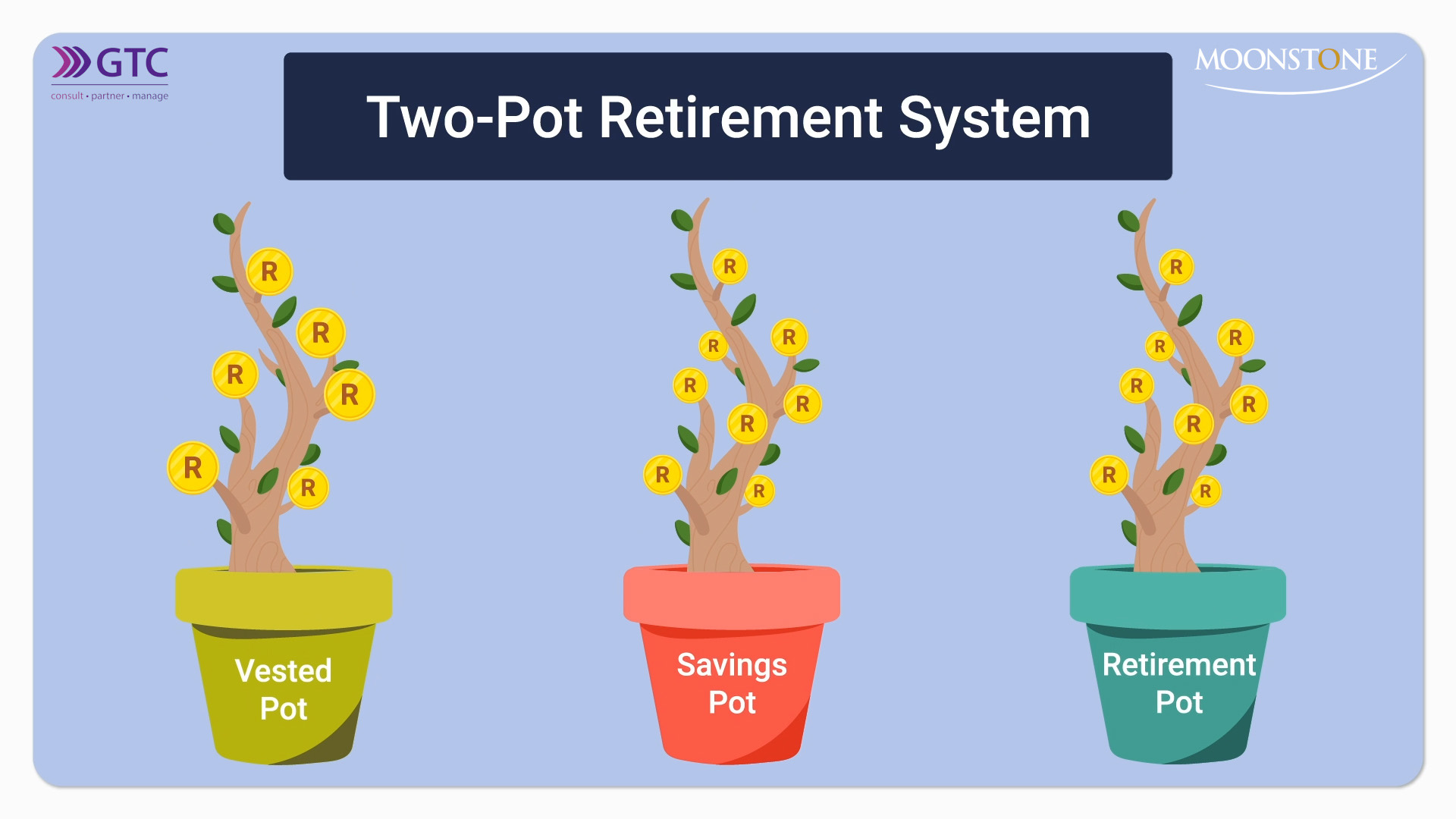

Two pots: administrators encouraged to submit draft rule amendments

The FSCA expects to receive a large number of amendments, so it would like to have prior sight of the proposed amendments beforehand.

The FSCA expects to receive a large number of amendments, so it would like to have prior sight of the proposed amendments beforehand.

Microinsurers are no longer restricted to imposing a waiting period of three months for a death, disability, or health event resulting from natural causes.

The exceptions to the exposure limits do not apply when the limits are breached because distributions are re-invested, the FSCA says.

The FSP conflated the requirements for debarment under section 14 of the FAIS Act with the requirements and procedure for a debarment by the FSCA.

The inherent risk of money laundering and terrorist financing for CASPs in South Africa is high, the report says.

The entities will co-operate to improve the level of submission of compliance reports.

The reasons for the sanction are virtually identical to those that saw the Authority fine an FSP earlier in February.

The 75% investment limit in Board Notice 52 inadvertently excluded the establishment of retail feeder hedge funds as a portfolio style.

Implementing – not merely creating – a Risk Management and Compliance Programme is crucial to ensure compliance with the Act.

The Authority’s findings in respect of an investigation have no legal consequences, the FST says.

The 13th Allianz Risk Barometer reveals that deepfake video technology, aimed at facilitating phishing scams, is now readily available online, priced as low as R377 a minute.

The FSCA encourages the public to be cautious of fraudulent schemes on messaging platforms, as they are on the rise.

The information will help the Authority to monitor the extent to which insurers are delivering fair outcomes for consumers.

The Full Bench of the High Court finds that the Authority’s investigating panel did not treat Michael Deighton unfairly.

An offer to assist the investor with recovering her returns from the individuals who defrauded also turned out to be a scam.

The Authority breaks down the red flags that may indicate a product or scheme is fraudulent.

Livestock Wealth says it was under the impression, based on correspondence with the Authority, that it did not need a licence to sell agricultural assets.